Māyā

Ideas written here were built on Jez's, Travis Kling's, Chumbawamba22's and Ray Dalio's work.

In Hindu philosophy, māyā is the veil that makes the contingent appear eternal. It is the power that persuades us to mistake appearance for reality.

For much of the twentieth century, the Western middle class lived inside its own secular māyā. The postwar settlement of stable employment, rising wages, affordable housing felt natural. A blessed alignment of policy, demographics and geopolitics fueled the dream.

Get a degree. Get a good job. Buy a house. Start a family. Retire safely. It was presented as reality itself rather than what it was. It felt permanent. It felt like the structure of the world.

It was only ever a moment.

The middle-class dream is ending. Not in a single country or economy, but everywhere. The same mega-trend, playing out at different speeds but in the same direction: job security weakening, income stagnating relative to asset prices, the cost of a normal life pulling further and further away from what a normal salary can buy.

The math no longer adds up, and everyone under forty can feel it even if they can't articulate exactly why. The veil is thinning. What lies behind it is not comforting.

Two Paths

When the promise breaks, people do one of two things. Gamble harder, or opt out entirely.

Jez, writing in oldcoin bad, calls this "long degeneracy": a belief that the world will only get more degenerate, financialized, speculative, lonely, tribal and weird. His thesis is clean: as real returns compress, risk increases to compensate.

Travis Kling, writing on Epsilon Theory, arrives at the same place from a different angle: "financial nihilism," the recognition that cost of living is strangling most people and upward mobility is slipping out of reach, driving a generation toward outsized risk-taking as the only rational response.

Both are right. And the numbers back them up.

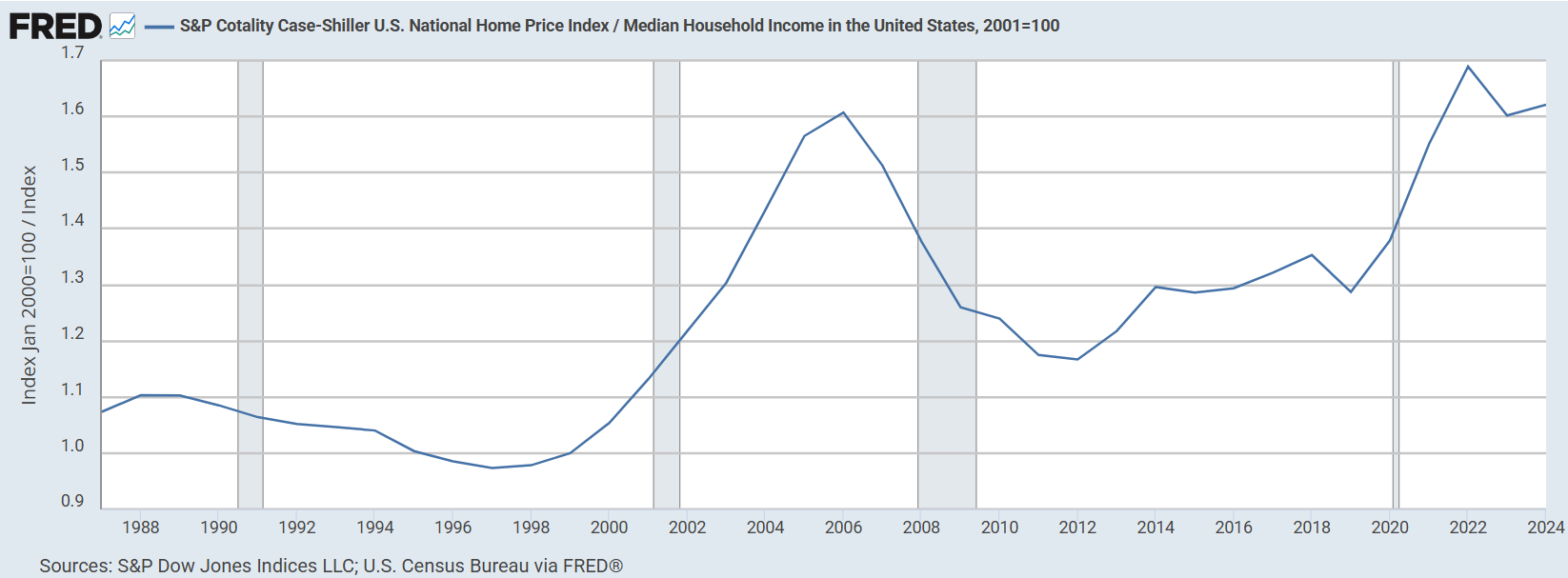

As of 2025, the median American home costs $416,900, 5x the median household income of $83,730. In the 1990s, that ratio was 3.2x. In 1985, it was 3.5x. Between 2019 and 2024, home prices rose 48% while median income rose just 22%. In Los Angeles the ratio is 12.5x. In San Jose, 10.5x. In New York, 9.8x. In 2019, 59 metro areas had price-to-income ratios below 4.0. By 2024, that number had collapsed to 25.

The affordable markets are vanishing.

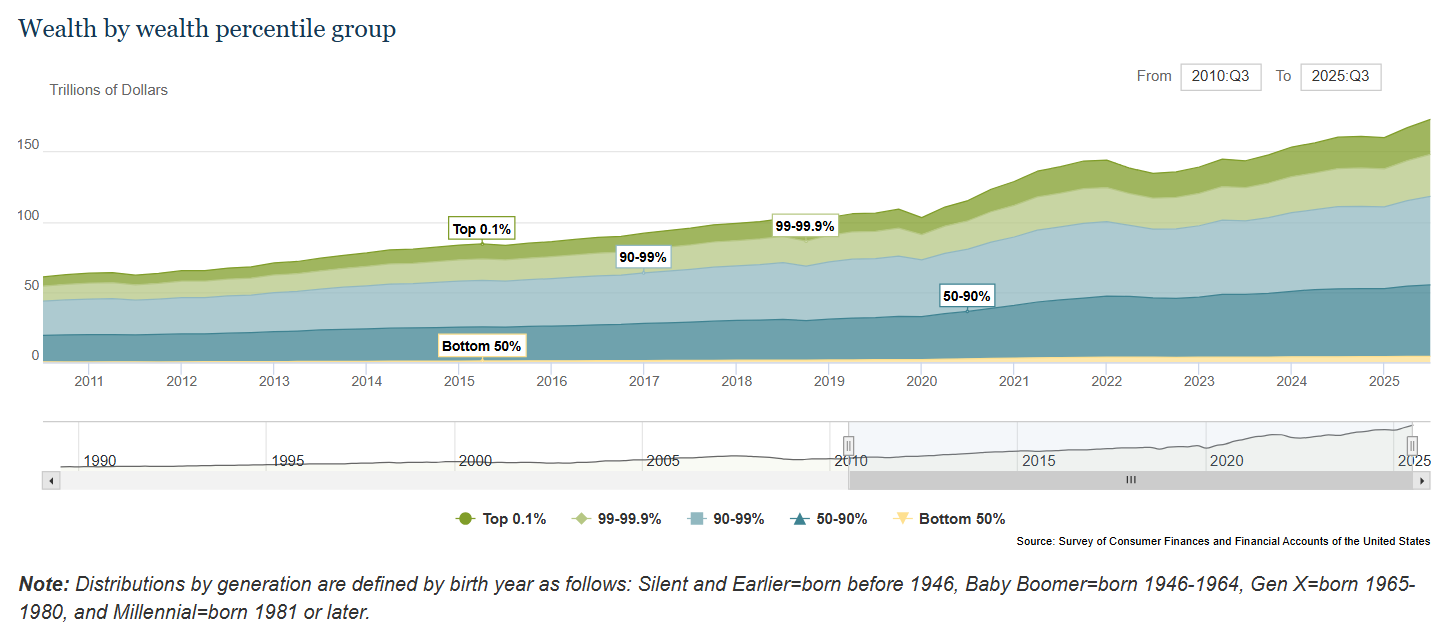

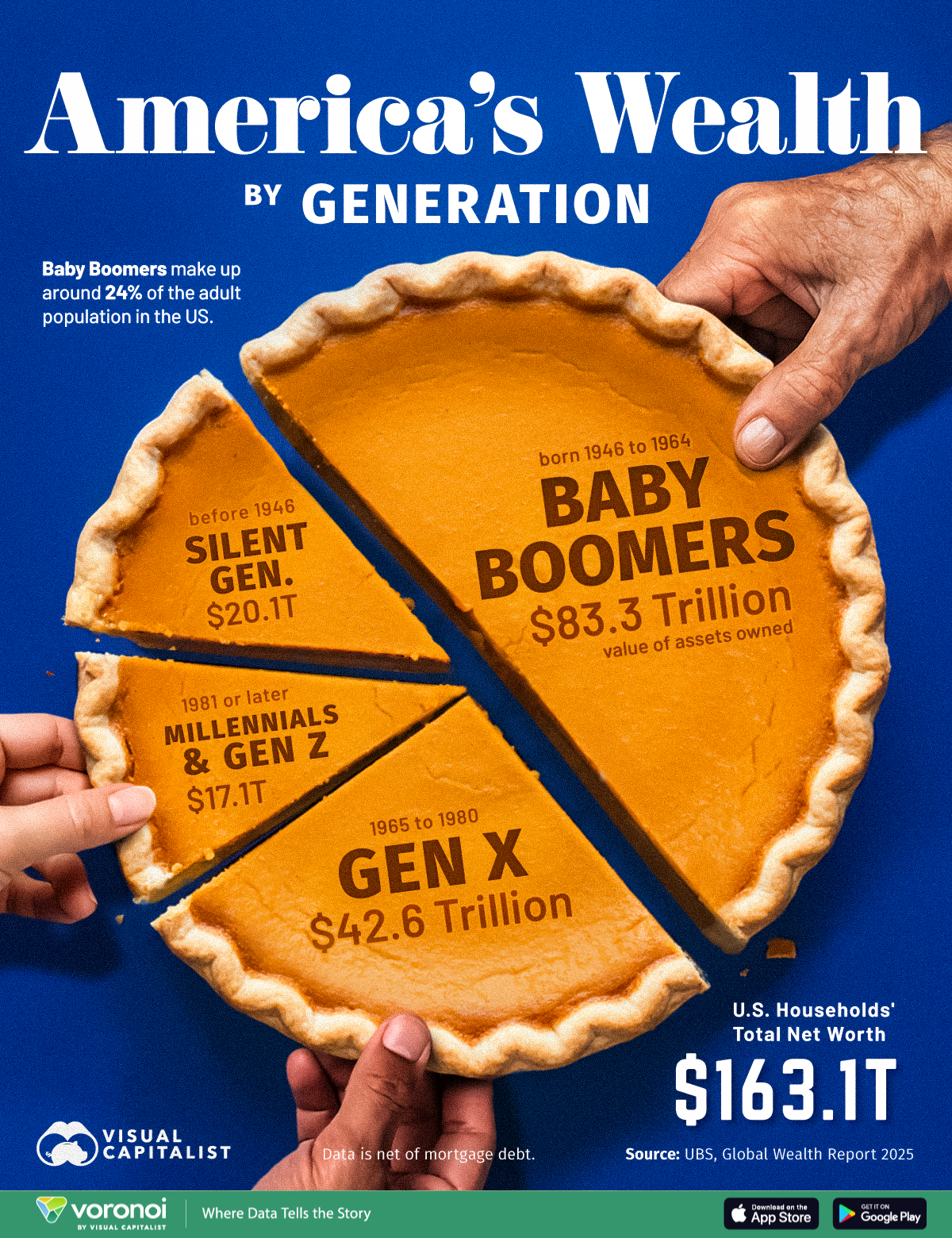

The wealth distribution tells the same story. As of Q1 2025, baby boomers hold 51.4% of total US household wealth. Millennials, a roughly equal share of the population, hold 10.3%. The top 10% of households own 67.2% of all wealth. The bottom 50% own 2.5%.

Within the millennial generation itself, the top 10% hold 69% of their cohort's wealth, up from 61% among boomers at the same age. Even the generation that is supposedly "catching up" is doing so only at the very top. The rest are falling further behind.

The response was gambling at unprecedented scale. Americans legally wagered $149.9 billion on sports in 2024, up 23.5% from the year before. Through the first eleven months of 2025, total commercial gaming revenue reached $71.49 billion, up 8.7% year-on-year. The 2025 Super Bowl alone generated $1.39 billion in legal wagers. DraftKings, just one operator, posted $6.05 billion in revenue for 2025, up 27% from the prior year, with $53.6 billion in sportsbook handle and 4.8 million monthly unique payers. They achieved their first-ever annual profit.

Meanwhile, prediction markets exploded. Polymarket and Kalshi generated a combined $44 billion in notional trading volume in 2025, up from $9 billion the year before. Polymarket processed over 95 million transactions. Its monthly active users surged from roughly 4,000 to over 600,000. DraftKings launched its own predictions app in December 2025, calling it a potential $10 billion annual revenue opportunity. Their CEO described prediction markets as the most exciting growth opportunity since sports betting was legalized in 2018. The casino is on your phone, the prediction market is on your phone, and both are open 24/7.

The speculation is not confined to casinos. Robinhood, the platform that democratized retail trading, posted record revenue of $4.5 billion in 2025, up 52% year-on-year. Equity trading volumes hit all-time highs, with $647 billion in a single quarter, up 126% year-on-year. Total platform assets surged 68% to $324 billion. The company joined the S&P 500 in September.

Pump.fun, the Solana-based memecoin launchpad where anyone can create a token in seconds for under two dollars, has processed over $150 billion in cumulative trading volume since launching in January 2024. Over 13 million tokens have been created on the platform. It hit $100 million in fees in just 217 days, faster than any crypto protocol in history.

Only about 1.4% of tokens ever graduate past their initial bonding curve. More than 60% of traders end in the red. They keep playing anyway.

This is financial nihilism in motion. But look at the macro dashboard and you would never know.

US GDP grew at 4.3% in Q3 2025, the strongest quarter in two years. Asset prices are at all-time highs. Unemployment, until recently, was historically low. On paper, the economy is booming.

But consumer confidence has cratered nearly 29% year-on-year, hitting a 12-year low. The Conference Board's Expectations Index has spent twelve consecutive months below the 80-point threshold that historically signals recession.

This is not an American anomaly. UK consumer confidence remains deep in negative territory despite two years of real wage growth, with household saving rates at their highest since 2015 as consumers hoard cash rather than spend. Eurozone consumer sentiment has been persistently negative throughout 2025.

The rot is beneath the surface. GDP measures aggregate output and this is increasingly driven by the top of the distribution. The wealthy are spending, asset-rich boomers are compounding, and the headline numbers reflect their economy, not everyone else's.

The active response is hypergambling.

"long degeneracy is your college friend sports betting. long degeneracy is your uncle trading options. long degeneracy is your participation in an online community instead of an irl one. these trends are modern efficiency applied to human nature — the shortest-term reward cycles." — Jez, oldcoin bad

Crypto, meme coins, 0DTE options, sports betting parlays, leveraged positions that either change your life or evaporate by Friday. It is an entire generation treating their paychecks as chips, because the alternative is saving for twenty years toward a house that costs more every month they save.

This is not a free layup. Most participants lose, and they know it. But when the alternative is thirty years of saving toward something that moves further away every year, the math of a long shot starts to feel less irrational.

But there is a quieter response too. The ones who look at the same broken math and decide not to play at all.

Tang ping, or lying flat. The Chinese phenomenon of young people withdrawing from the rat race entirely, doing the bare minimum, refusing to participate in a system that offers diminishing returns on effort.

DINKs choosing not to have kids, not always by preference, but because economics of raising a family have become irrational. Rising structural unemployment among the young, not because of no jobs, but because jobs available no longer lead anywhere worth going.

This isn't laziness or apathy but rational responses to a broken social contract. If effort no longer reliably converts to outcome, why burn yourself out pretending it does?

Culture itself reshapes and reflects this. When traditional status goods like houses, cars, and luxury watches become unattainable, status migrates to new things. People find new ways to signal within their means, and new consumer trends emerge.

Look at the Labubu and PopMart craze. Collectible figurines sold in blind boxes where you don't even know which one you're getting. Gambling mechanisms are baked directly into the purchase. The same logic drives the resurgence of Pokémon and trading card games: sealed packs, chase cards, speculative grading, selling rare pulls at higher multiples.

The dopamine loop is identical. It is gambling and status consumption fused into a single product.

Look at how travel has replaced ownership as the dominant flex on social media. Young people aren't posting pictures of their houses or their cars. They're posting Bali sunsets and Tokyo street food. Experiences have become the status signifier, not because people philosophically prefer experiences over assets, but because experiences are the only flex still within reach.

Look at streaming and OnlyFans. Becoming a famous content creator, whether through gaming, lifestyle, or selling access to yourself, is the new aspirational career. High variance, parasocial, entirely financialized attention. It is the ultimate long degeneracy profession.

A tiny percentage make life-changing money. The vast majority make nothing. The distribution is pure power law. And yet they keep trying, because the expected value of chasing an audience for five years is, for many, genuinely competitive with the expected value of a mid-tier corporate career. That tells you everything about where the corporate career has ended up.

None of these are cultural quirks or generational preferences. Gambling harder, lying flat, redefining what success looks like. They are all downstream artifacts of the same broken economics, rationalized into lifestyle choices.

AI's Capex Trap: The Great Sorting

The recent boom in AI developments only accelerates the sorting. I believe most white-collar and SaaS work at scale are already in rapid danger of being displaced. The market has already moved and priced this in; look at the underperformance of the Mag7 relative to industrials, hardware and commodities. Premia on knowledge work is compressing in real time. The very jobs that were supposed to justify our degrees, debts and decades of grind are becoming substitutable.

The rate of change matters here. AI labs are now using their own models to build the next version, and the recursive self-improvement loop is real. The capability curve is going parabolic. Tasks that took frontier models hours two years ago now take minutes. The window for any skill-based competitive advantage is shrinking faster than most people realize.

And for those with high agency and access to capital, AI is a force multiplier of extraordinary power. One person with the right tools can now do what took a team of twenty. The distribution of successful outcomes sharpens from 80-20 to 95-5. Maybe worse. This is the K-shaped economy in its purest form: AI supercharges the winners and makes everyone else more replaceable.

Chumba wrote that the replacement math is not abstract. The fully loaded cost of a mid-level knowledge worker — salary, benefits, 401k match, medical, real estate allocation — runs roughly $150,000 per year. Eliminating that role accretes $1.2 to 2.5 million in equity value to the firm depending on your discount window. It is not a theoretical efficiency gain but the single highest-ROI capital allocation decision most companies can make right now.

AI hyperscaler companies have already crossed the inflection point. Free cash flow used to fund stock buybacks and powered the sixteen-year equity bull run is being redirected into AI capex. They are no longer capital-light cash cows but rather capital-intensive businesses that must reinvest to remain competitive. Cheap open-source and Chinese LLM alternatives are biting at their toes perpetually six to twelve months behind.

This spending itself automates away the white-collar workforce that have been bidding index funds via their 401ks for the past decade. Capital that once flowed back to shareholders is now funding their very own elimination.

Passive index flows from these contributions have grown from single-digit market share in the 2000s to roughly half the market today. However, if white-collar employment contracts (and the incentive math says it will), these flows unwind and whatever drove the market up will drastically correct downwards.

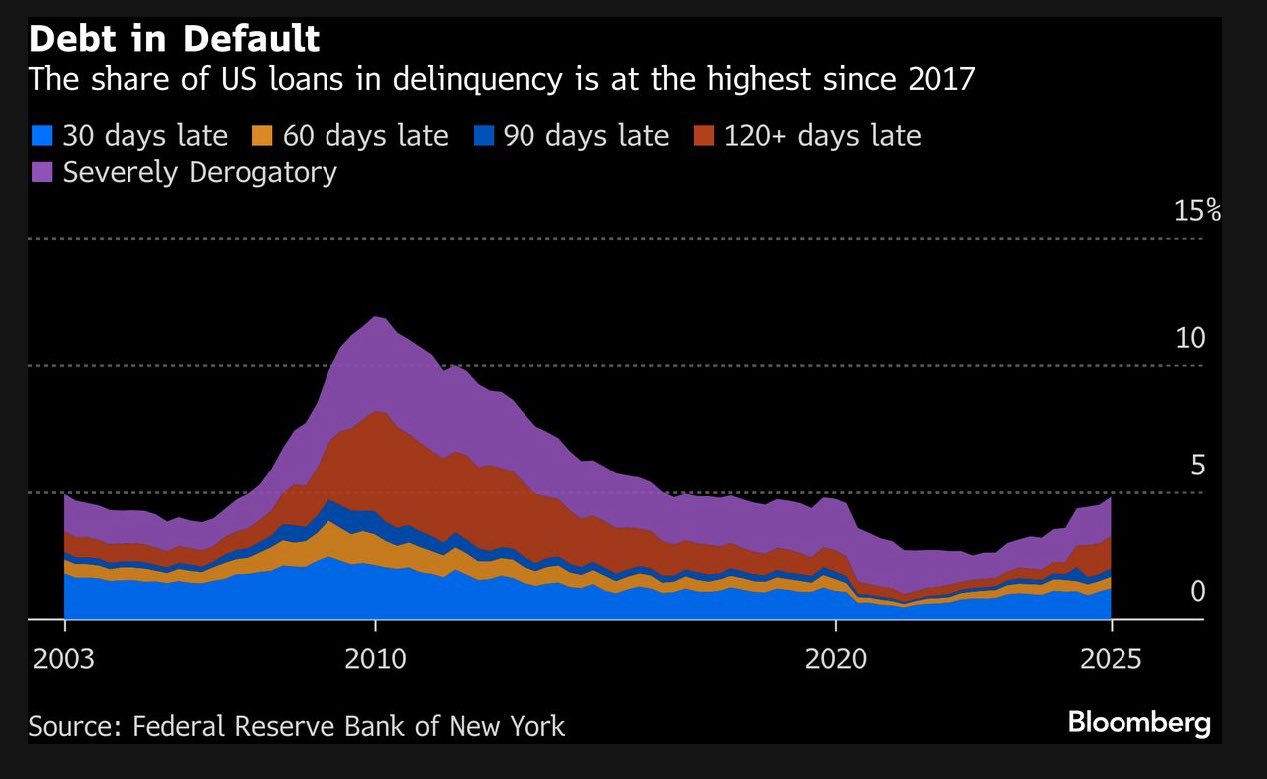

The stress is already visible at the consumer level. US retail sales unexpectedly stalled in December 2025, dragged down by declines in clothing and furniture — discretionary spending, the first thing to go when household budgets tighten.

Meanwhile, the share of US loans in delinquency has climbed to its highest level since 2017, per the Federal Reserve Bank of New York.

A contradiction worth pointing out here is that the financial nihilism thesis implies risk-on behaviour; people are slamming capital into random stocks, crypto, memes, 0DTE options, sports parlays and anything with asymmetric upside. The nihilistic bid in aggregate pushes participants into these very risk assets.

However, the buybacks that powered the bull run are being redirected into AI capex and the passive flows that inflated large-cap indices depend on the very employment that AI is designed to eliminate.

A new Warsh Fed regime also signals a higher threshold for liquidity intervention and tightening. The institutional bid itself is thinning. What remains is the retail nihilist, gambling harder than ever before. Nominal highs in asset prices only mask the fact that the foundations have changed.

This is the trap within the trap.

Financial nihilism sustains the illusion of healthy markets precisely long enough for late stage retail to get trapped.

However, financial nihilism and the bear case are not opposing views, but on different timeframes; the gambling sustains the surface until market shock removes the gamblers themselves. You cannot bet your paycheck if you do not have one!

So who is right? The degens or the bears? Both.

The degens are correct that the expected value of conventional saving is broken and that asymmetric bets are individually rational. Bears are correct that the aggregate structure cannot hold. Ultimately, financial nihilism is the last leg of a table whose other legs have already been sawed through, and it is already giving way.

The Macro Trap

The global order is restructuring: institutional decay, erosion of post-war frameworks, a kind of reverse Perestroika. More on this another time. For now, the financial architecture underneath.

Ray Dalio's big debt cycle describes a pattern that has repeated across every major empire and reserve currency in history. The arc is always the same. Early in the cycle, debt is productive: it funds growth, infrastructure, expansion. Debts are manageable relative to income. The system works.

But over time, debt grows faster than the income needed to service it. Governments borrow more to cover obligations. Central banks accommodate. The cycle matures.

We are in the late stage.

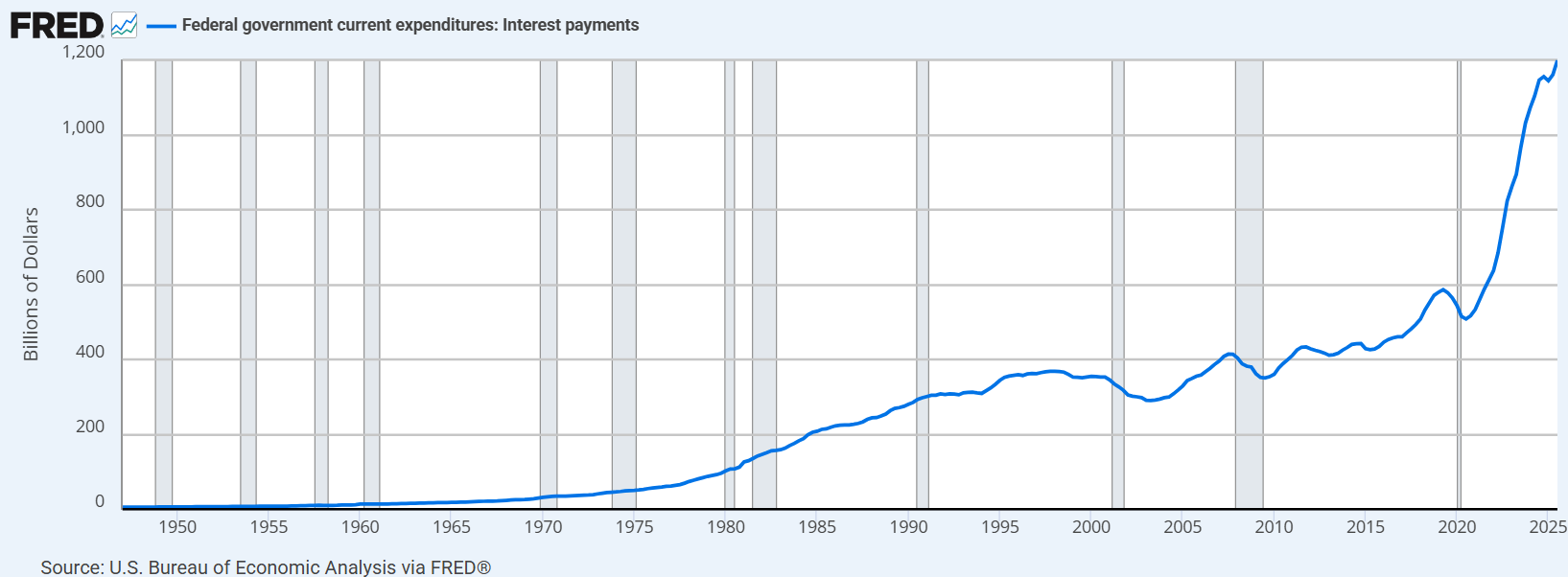

Sovereign debt levels across major economies like the United States, Japan, China, and Europe are at historically unsustainable levels. The US national debt exceeds $36 trillion. Interest payments on that debt are now one of the largest line items in the federal budget, competing with defense spending.

The debt-to-GDP ratio has entered territory that, historically, no major power has exited without significant upheaval, whether through inflation, default, restructuring, or conflict.

And the central banks are trapped.

They cannot raise rates without crashing asset markets built on cheap money. They cannot cut without debasing the currency further. Both paths worsen inequality and erode the purchasing power of anyone who holds cash or earns wages rather than owning assets.

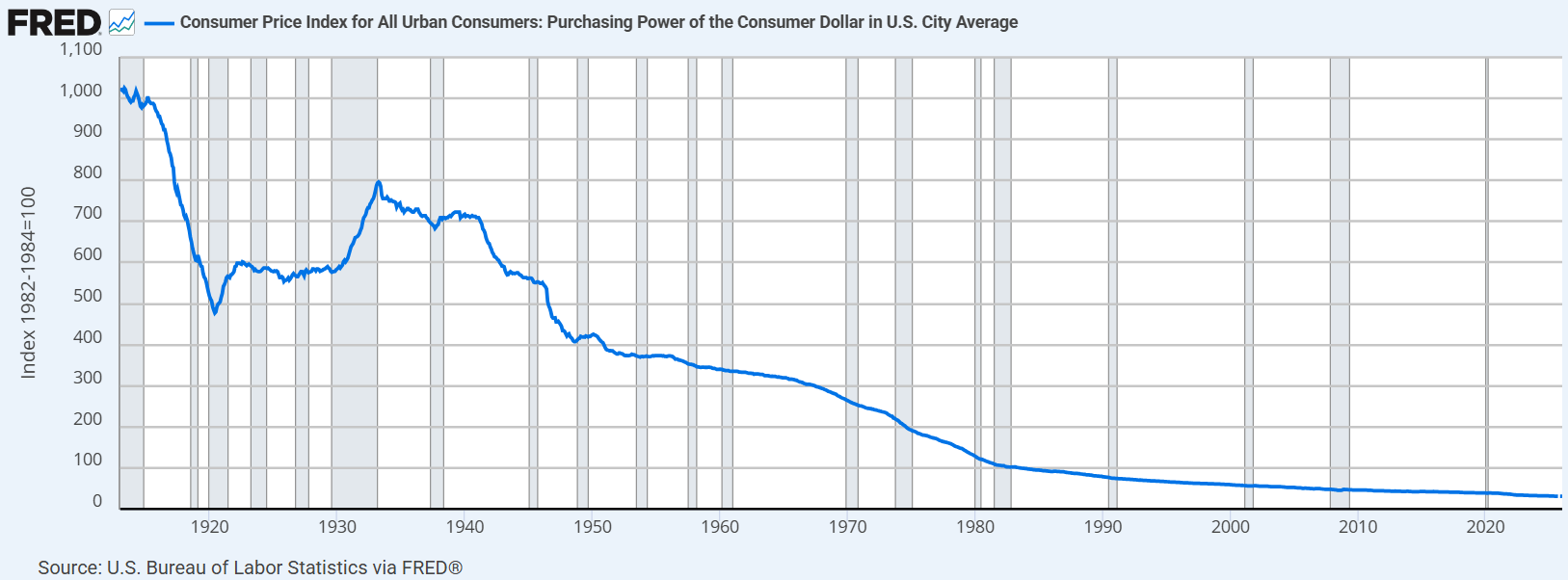

So the only tool left is financial repression: keeping real yields negative, letting inflation quietly erode the debt while punishing savers. The same playbook used in the late stages of every debt cycle Dalio documents. The currency is going to zero, just slow enough that most don't notice, but fast enough that those without hard assets fall further behind every year.

Even a hawkish Warsh Fed only delays this. The debt math overrides any individual regime; tightening continues until something breaks (made worse by AI deflation), and then the printing resumes harder than before.

The gold market has priced this in with an almost violent clarity. Gold rallied 66% in 2025, its best year since 1979, blasting through $4,000 an ounce for the first time in October and closing the year near $4,325. Silver was even more extreme, up over 140%.

As of early 2026, gold has breached $5,000 and silver briefly broke $100 in January before a violent sell-off brought it back to the low $80s. JP Morgan, Goldman, and Citi have all been forced into repeated upward revisions, their targets overtaken before the ink is dry.

Central banks purchased over 1,000 tonnes of gold for the third consecutive year, diversifying away from US Treasuries. Gold's share of central bank reserves has surpassed Treasuries for the first time since 1996.

But it is not just sovereigns. ETF inflows and retail buying have surged. The bid is broad-based and global: Chinese insurance companies, Indian pension funds, Western retail investors who have watched fiat purchasing power erode in real time and decided to opt out.

This is the same impulse driving the sports betting boom, the retail trading surge, the memecoin launchpads, the prediction market explosion, and the record flows into gold. People are re-pricing risk and losing trust in the denominator.

Furthermore, gold itself has a ~5,000-year track record. When the retail herd and the institutional hedge converge on the same trade, it tells you something about the depth of the structural distrust today.

This is why asset prices keep rising in nominal terms while becoming less attainable in real terms. The house isn't getting more valuable. The money is getting less valuable. And the people setting monetary policy have no way to stop it without triggering the very collapse they are trying to avoid.

Dalio's framework explicitly links this stage to social instability. The wealth gap widens, internal conflict rises and populism surges on both the left and the right wing. Trust in institutions erodes. The social fabric frays.

The Endgame: Capital vs. Labor

Here is what sits underneath all of this.

Capital markets increasingly reward those who allocate capital over those who produce through labor. This is not new; capital has always earned more than labor over long time horizons. The gap is accelerating, and the disparity is widening faster than ever. And it explains nearly every trend in this essay.

Selling your time no longer provides the upward mobility it once did. A generation ago, a competent professional could reasonably expect that trading forty hours a week for a salary would, over twenty or thirty years, compound into a house, a retirement fund, a stable life.

That was the heart of the māyā: the belief that effort and time would be enough.

The causal link between effort and outcome is broken. Not completely yet, and not for everyone, but for enough people that culture and capital have already shifted in response.

But even those who win are not safe. Most of the value flows upward to platforms and infrastructure owners. And the few who cross over from labor to capital are betting on markets whose direction depends on the very buybacks and employment flows that AI is eating.

And this is where the K-shaped economy reaches its logical conclusion.

The economy bifurcates into two broad roles. On one side: those who own and allocate productive infrastructure: capital, platforms, technology, hard assets. On the other: the broader population, whose economic relevance is no longer tied to productivity but to participation, consumption, and legitimacy.

Some do cross the gap. Some speculators hit the jackpot, some founders break through, a handful of content creators go viral and monetize it before the window closes.

But the existence of lottery winners does not change the structure of the lottery. Visible success stories keep millions more playing a game where the expected value is negative. They are the marketing.

Read that again.

People are no longer paid primarily for their work. They are compensated because the system is productive enough without them, and it requires social stability to function.

Wages, benefits, and eventually perhaps Universal Basic Income are not payments for contribution. They are the cost of maintaining a consumer base and preventing the whole thing from eating itself.

Even if UBI were implemented perfectly, it would not resolve this bifurcation but only strengthen it. A guaranteed stipend only cements the gap between the allocator class and everyone else, and if you can try again next month, what's the downside of speculating with this month's check?

Let us call a spade a spade. We are in neo-feudalism.

The allocator class owns the land and the infrastructure. Everyone else works within their systems, or does not work at all, sustained by the modern equivalent of a lord's rations, kept stable enough to consoom and not revolt. Different language, same caste system.

Here is the uncomfortable truth that nobody wants to say out loud: the middle class dream was an anomaly and not the norm. A brief historical window, born from the post-war boom, cheap energy, a global labor arbitrage, and a one-time expansion of the economic pie, convinced an entire civilization that broad-based prosperity was the natural state of things.

This trend has broken and we are regressing to the mean. A world of hierarchy. A world of winners and losers. A world of serfs and lords.

"And there have always been and there always will be the same percentage of winners and losers. Happy foxes and sad sacks. Fat cats and starving dogs in this world. Yeah, there may be more of us today than there's ever been. But the percentages, they stay exactly the same." — Jeremy Irons, Margin Call

There is a bitter paradox at the root of all of this. Every individual rational response: gambling harder, opting out, redefining status, chasing asymmetric upside, collectively deepens the very conditions that created the trap.

The more people speculate, the more value flows to the capital side. The more people lie flat, the less political pressure exists to change the structure. The more status migrates away from traditional markers, the easier it becomes to mistake the cope for the cure.

The Veil Lifts

The forces described in my post are not independent phenomena. They are converging, reinforcing each other, and accelerating.

Māyā is dissolving. The illusion that hard work and patience would be enough, that the system was built for you, that the ladder was still there if you just kept climbing.

None of it was true.